Washington, DC - In a time of digital acceleration, government expansion, and economic friction, one fundamental question quietly powers through the haze:

Who decides what borrowed money is worth?

Is it a panel of unelected technocrats at the Federal Reserve? Is it the executive branch, reflecting the will of the voters? Or should interest rates function like the price of gas — responsive, visible, shaped by supply, demand, and basic economic gravity?

The fight over interest rates — now more public and political than it’s been in decades — is no longer just about inflation, growth, or bond yields. It’s about power, democracy, and reality itself.

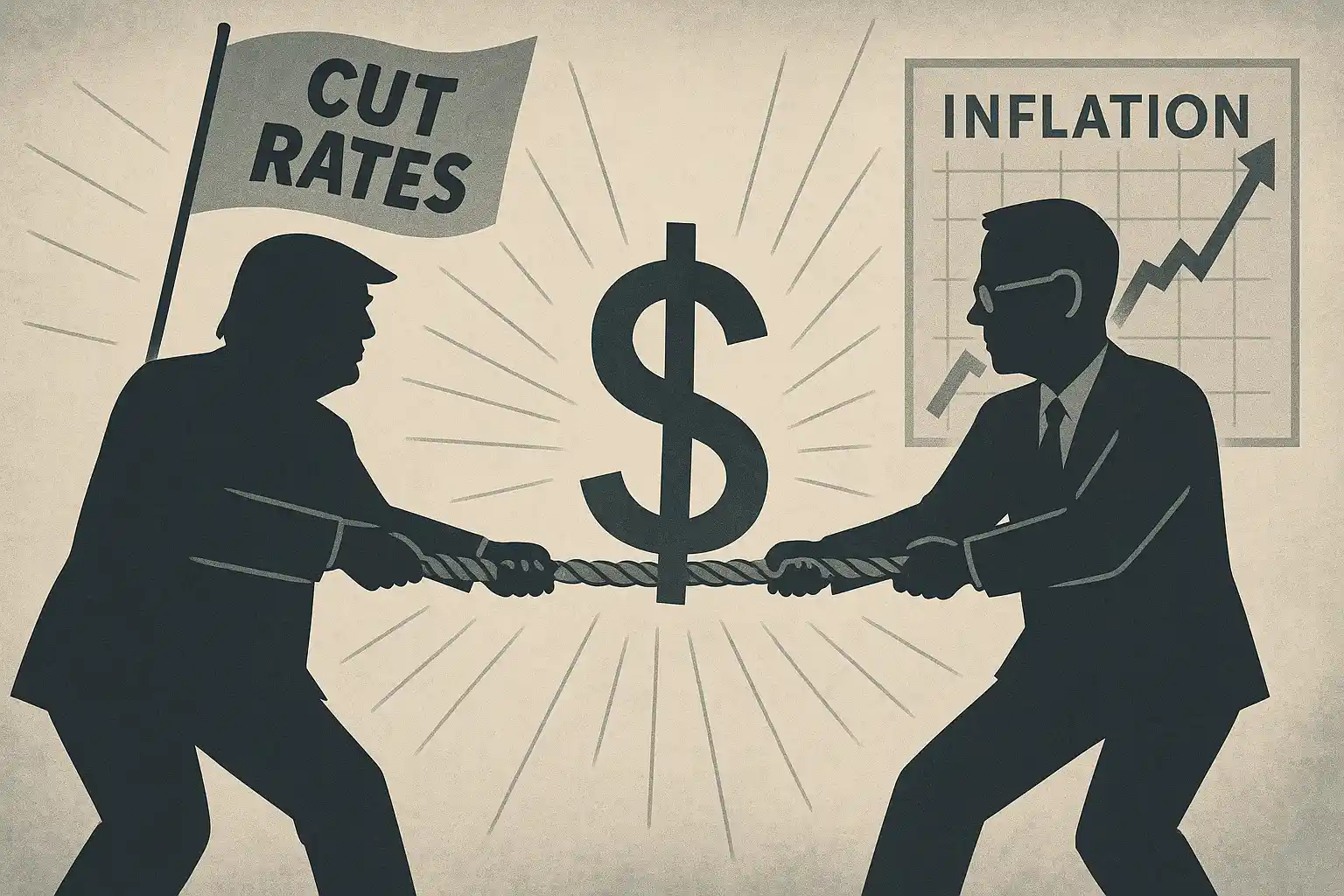

President Donald Trump is now openly calling for deep rate cuts — down to 0.5% or even 0%, a return to emergency-level borrowing costs in the name of growth and relief. His argument? High interest rates are choking the economy, hurting homeowners, and killing momentum.

The Federal Reserve, led by Chair Jerome Powell, is resisting. Citing persistent inflation risk and concerns over political pressure, the Fed has kept rates elevated — currently hovering in the 2%–3% range.

The fight is no longer academic. Trump allies are lining up for potential Fed appointments. Some, like Fed Governor Christopher Waller and Governor Michelle Bowman, have already signaled openness to faster cuts. Others will press the institution hard to fall in line with the executive agenda.

The debate over rates reveals something deeper and older:

Who decides what money is worth — and who gets to say how much it costs to borrow it?

Because interest rates aren’t just economic levers. They are the price of time, the gatekeeper of opportunity, and the silent force behind debt, growth, investment, and retirement.

Right now, that price is set by the Federal Reserve — an independent central bank, designed specifically to act above politics.

But here’s the contradiction: money is a public medium, yet its value is dictated by a private panel. It touches every life, yet is controlled by none of them directly.

Should that continue?

Fed defenders argue that central bank independence is essential for long-term stability.

In this view, the Fed is the “adult in the room” — tasked with price stability, not political popularity. It has the tools, the models, the mandate.

Let the voters run everything, the argument goes, and you’ll get hyperinflation, moral hazard, and crisis.

And there’s some truth to that — we’ve seen it before, in Argentina, Venezuela, Zimbabwe.

But America isn’t those countries. And its population — enormous, industrious, and restless — might no longer be satisfied with total monetary outsourcing.

America isn’t just an economy — it’s a republic. And its people are waking up to the fact that the price of money shapes almost every element of their lives:

Yet they have zero direct say in how that price is set.

The idea of monetary democracy is radical to some — but maybe that’s because we’ve normalized technocracy.

Should we at least have more transparency, or a blended system where markets compete to set rates, like gas prices? Should the executive branch — elected by tens of millions — have more direct influence over rates during economic emergencies?

Or does that open the floodgates to manipulation and economic collapse?

There’s no simple answer. But the question is real. And growing.

Let’s imagine a different world:

Oversight still exists — transparency, anti-fraud enforcement, capital requirements.

But the price of money floats, grounded in real trust and risk — not in a closed room full of models and forecasts.

This isn’t fantasy. It’s how lending used to work — and how many still believe it should.

If the Fed caves under political pressure, credibility suffers. Markets smell weakness. Bondholders demand higher yields. The dollar may wobble.

But if the Fed never responds to democratic will — or worse, becomes a self-reinforcing priesthood — then faith in the entire financial order erodes from the inside.

We’re watching this play out in real time:

And they wonder:

“Who are these people? And why do they get to decide how hard I have to work to keep up?”

There’s no simple solution. But there is a core truth:

Money belongs to the people who use it. Not just the ones who issue it.

We can have a central bank. We can have a monetary policy. But maybe — just maybe — we should also have a system where the people’s voice, the real economy, and the price of time aren’t so disconnected.

Because if rates are always controlled from the top down, the question isn’t just "how much does it cost to borrow?"

It’s: Who are we borrowing from — and who really holds the power?